Finance & economics | Marginalia

Why China’s central bank won’t save the country from deflation

It’s not about the exchange rate any more

February 12th 2026

FOR DECADES Americans have fretted that China might dump its vast holdings of Treasuries, undermining the dollar. Global investors therefore snapped to attention when Bloomberg, a news agency, reported on February 9th that China’s regulators have warned commercial banks against holding too many American government bonds. Some banks have been told to cut their exposure. In response to the news, the dollar fell against China’s yuan and Treasury prices wobbled.

Are fears of Sino-American financial warfare finally coming true? Thankfully not. In guiding its banks, China was not making a fresh geopolitical threat. At most, it was trying to limit the banks’ vulnerability to the many geopolitical threats that already exist. Dollar bonds have been a tempting asset for Chinese lenders, offering higher returns than similar securities at home. But any hit to the dollar could inflict heavy losses on overexposed lenders.

No wonder China’s authorities feel nervous. As well as hurting the banks, a weaker, more competitive dollar will curb the appeal of China’s exports, a vital source of growth. Together with cheaper imports, that could also worsen China’s deflationary tendencies. According to figures released on February 11th, consumer prices rose by only 0.2% in the year to January. The falling cost of pork (down by 14%) offset the rising price of bling (gold jewellery increased in price by 77%). An alternative measure of prices as charged at the “factory gate” has been falling for years.

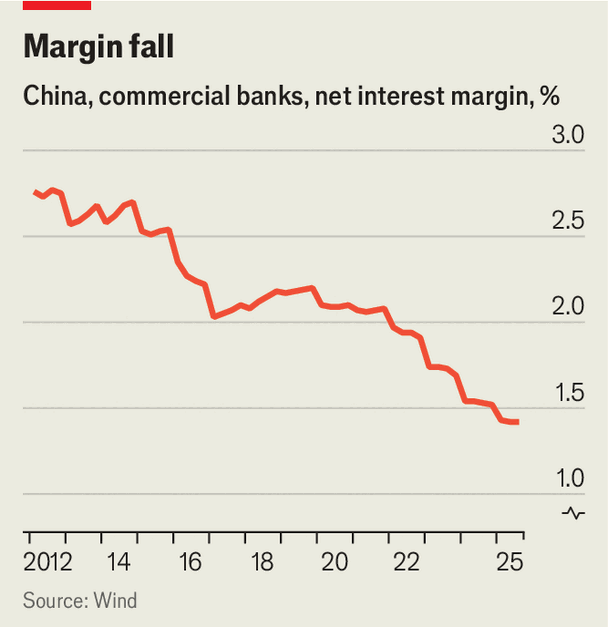

Although recent currency movements could worsen this problem, they remove a troublesome constraint on the central bank. In the past, worries about the yuan have prevented the People’s Bank of China from aggressively cutting its policy interest rate, which has remained at 1.4% since last May (see chart). It feared that monetary easing would add to downward pressure on the currency. Now that would probably be welcome. “The exchange rate doesn’t pose a strong constraint overall,” said Zou Lan, deputy governor of the central bank, at a press conference last month.

Unfortunately, another obstacle remains: bank profitability. Banks make money by borrowing cheaply and lending more expensively. But in China the margin between deposit rates and lending rates is at a record low of 1.4%, far below the 1.8% recommended by regulators. To win business, banks are sometimes tempted to underprice their loans and overcompensate their best depositors. The central bank worries that disorderly competition (or “involution”, as the Chinese call it) now afflicts the country’s financial institutions, just as it plagues manufacturers, e-commerce firms and high-school exam-takers.

Mr Zou hopes that this pressure will ease this year. Many three- and five-year deposits will mature in 2026, allowing banks to reprice them at lower rates. That should allow the central bank to reduce its own policy rate, but not by much. Most economists expect it to make just one or two cuts of 0.1 percentage points each.

The central bank might ease more if the economy deteriorates. If growth looks like it will fall short of this year’s official target (which will probably turn out to be 4.5-5% when revealed next month) the central bank will recalibrate. It is in “wait-and-see” mode, says Helen Qiao of Bank of America. She cites an old Chinese idiom (ke zhou qiu jian) which refers to a hapless traveller who loses their sword overboard when crossing a river. To mark the spot, they foolishly carve a notch in the side of the boat. Ms Qiao trusts that China’s central bank will not make the same mistake.

If the economy weakens further, the People’s Bank will be quicker to dive in. But perhaps not quick enough. According to some measures, China fell into deflation over two years ago. There has been a lot of water under the bridge since then. ■

For more expert analysis of the biggest stories in economics, finance and markets, sign up to Money Talks, our weekly subscriber-only newsletter.