The Americas | The grind

Brazil’s economy is being throttled by entrenched interests

The country should be faring much better

February 12th 2026

The outcome of Brazil’s general election in October will hinge on two issues: crime and voters’ purses. President Luiz Inácio Lula da Silva, known as Lula, is betting the economy will win him re-election. Annual growth at around 3% has outpaced expectations for three years. Annual inflation of 4.3% is trifling by Brazil’s standards. Unemployment is at a record low.

Yet the opposition paints a grim picture. Tarcísio de Freitas, the right-wing governor of São Paulo, says the country is in a “fiscal crisis”. Financial pundits warn of an imminent recession. “We’re not in the intensive-care unit, but we are moving towards that,” says Armínio Fraga, a former boss of Brazil’s central bank.

How sick is the patient? Brazilian debt is unsustainable on its current path. According to the IMF, gross public debt will hit 99% of GDP in 2030, up from 62% in 2010. The current debt is 30 percentage points higher than the median rate among emerging markets and Brazil’s Latin American peers. The nominal deficit is a whopping 8.1% of GDP, composed almost entirely of interest payments. The doomsayers are right to forecast trouble.

Businesspeople in São Paulo blame a generous welfare state and Lula’s loose purse strings. They have a point. When he came to power in January 2023, Lula inherited a primary surplus equivalent to 1.4% of GDP and a total deficit of around 4.5%. By December 2025 the government was running a primary deficit of 0.4% of GDP. The direction of travel has lowered market confidence in the government’s ability to limit the debt. This has forced the central bank to hold real interest rates near 10%—among the world’s highest—crowding out private investment and constraining growth. Brazil invests just 17% of GDP, barely half the rate of India.

But Brazil’s problems go far beyond Lula’s profligacy. Its economy is also degraded by the ability of powerful groups to wangle benefits from whoever is in government—many of them written directly into the country’s interminable constitution. Whether Brazil can meet its potential depends on whether lawmakers elected in October find the courage to stand up to entrenched interests.

Handouts are often blamed, but are a red herring. They cost a reasonable $83bn, or 3.7% of GDP, per year. This includes a flagship programme, Bolsa Família, which pays poor families to vaccinate their children and keep them in school, as well as various disability and unemployment benefits. Spending on public health and education, at around 4% of GDP each, is in line with that of Brazil’s peers. “I am a classical liberal,” says Mr Fraga, “but cutting spending in health and education in Brazil would not be my priorities.”

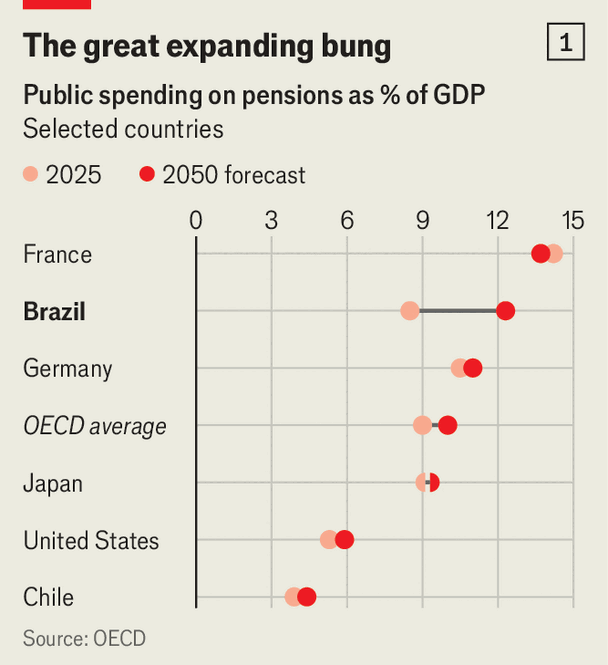

The behemoths dogging the economy are pensions and a dizzyingly complex tax code. Pensions cost the government 10% of GDP. If no reforms are made by 2050, Brazil will spend more on pensions as a share of GDP than many richer and greyer countries (see chart 1). Though Brazil’s share of young people is similar to that in Chile or Mexico, its pension spending is already at Japan’s level. That is despite a modest reform in 2019 that introduced a minimum retirement age. The population is ageing rapidly. Without reform, its social-security deficit, or the shortfall between contributions and payments, is set to rise from 2% of GDP today to over 16% by 2060.

Much of this money is gobbled up by a coddled public sector. Brazil has around 13m public employees and 40m formally employed private ones, yet the social-security deficits for the two systems are virtually the same. This makes Brazil a global outlier. Juicy perks draw the most educated workers into government. Their giant pensions are thus a subsidy for Brazil’s rich.

The judiciary and the armed forces get the biggest bungs. Brazil’s courts cost 1.3% of GDP—the second-most expensive in the world—mostly because of generous pensions. The typical soldier retires before turning 55 on a pension equivalent to their full salary. “We need to do ambitious structural reforms, like pension reform, from the top down,” says Dario Durigan, the deputy finance minister. “We can’t have huge pensions for the military and judiciary while cutting them for the little guy.”

It is fiendishly difficult to change the status quo, because reforming pensions requires changing the constitution. It mandates that pensions must rise in line with any increases to the minimum wage. Since every modern president—especially Lula—has put up the minimum wage, this has forced the government to keep boosting pensions. If pensioners get less than they feel they deserve, they can easily win in court. Each year the federal government loses the equivalent of 2.5% of GDP because courts order hefty pension and welfare payments.

Brazilian politicians have tried to get around these constraints by devising complex fiscal rules designed to limit government spending, in the hope that such gestures will win market trust. It hasn’t worked. Unless pensions are reformed, the market will never trust Brazilian fiscal rectitude. That distrust is costing Brazil between half and one percentage point of GDP growth annually, up to $250bn over the next decade if nothing changes.

The world’s most complicated tax system is also holding back growth. Brazil collects more tax revenue—around 34% of GDP—than most of its peers. But the system is a mess. Of 147 companies surveyed by Deloitte in Brazil last year, firms with annual turnover of up to $95m spent an average of 16,200 hours a year filing taxes. The largest firms, with sales greater than $1.5bn, spent 63,000 hours. Estimates of the economic costs vary, but it is on roughly the same order as the growth lost to lack of fiscal credibility, amounting to perhaps half a point of GDP annually.

Interest groups have obtained preferential treatment, creating fragmentation of the tax system and high compliance costs. The evolution of corporate income taxes is revealing. The headline rate is 34%, high by global standards. But few firms pay anything like that. The effective corporate tax rate is 16-18%, says Sérgio Wulff Gobetti of the Institute of Applied Economic Research, a public body linked to the budget office. That is one of the lowest figures among OECD countries.

Instead, most Brazilian firms are classified under special tax regimes. The so-called “Simples” scheme lets companies with annual sales of up to $900,000 pay as little as 4% tax on their revenue. Another allows companies with revenues of up to $14m to pay tax based on projected profits, rather than real ones. Both were meant to help small firms deal with taxes in a simplified way, but their thresholds were pushed so high that they in effect include most economic activity. Of Brazil’s 16.5m companies, only 220,000 pay the full rate of corporate income tax.

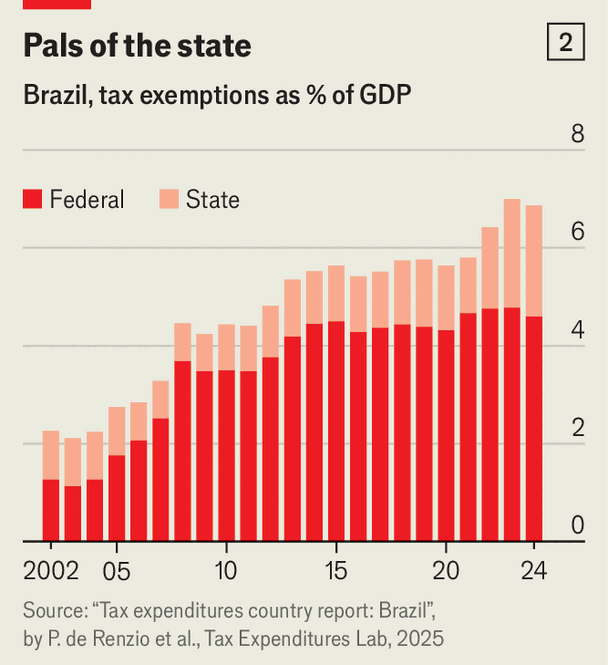

The country spends a staggering 7% of GDP on tax breaks, up from 2% in 2003, according to the Fundação Getulio Vargas (FGV), a university in São Paulo (see chart 2). Of 128 tax-break regimes, 95 are set to remain in force until 2073. The exemptions contribute to Brazil’s regressive tax system. The share of revenue from tax on corporate and personal income is 12 percentage points lower than the OECD average; most comes from taxes on consumption, which hit the poor disproportionately.

Lawmakers are aware of these problems. Since 2019, new tax breaks must expire within five years. A constitutional amendment passed in 2021 says tax breaks should cost no more than 2% of GDP by 2029. Another in 2023 simplifies the morass of consumption taxes into a dual VAT system. That also could boost GDP by up to 4.5% by the time it is fully implemented in 2033, according to FGV research.

Most reforms have, unsurprisingly, been riddled with carve-outs. The Simples regime and the Manaus Free Trade Zone, a failed industrial policy that gives the Amazonian city a gigantic tax waiver to produce white goods, have been excluded. Both are enshrined in the constitution. Corporate and payroll taxes are largely untouched. Pension reform is political dynamite. Unless politicians find the courage to clean up, Brazil will stagnate into crisis. ■

Sign up to El Boletín, our subscriber-only newsletter on Latin America, to understand the forces shaping a fascinating and complex region.